Most used cars sold in the UK have had PCP finance on them at some point. Understanding how it works tells you what risk you are taking if the seller has not paid it off.

How PCP Works

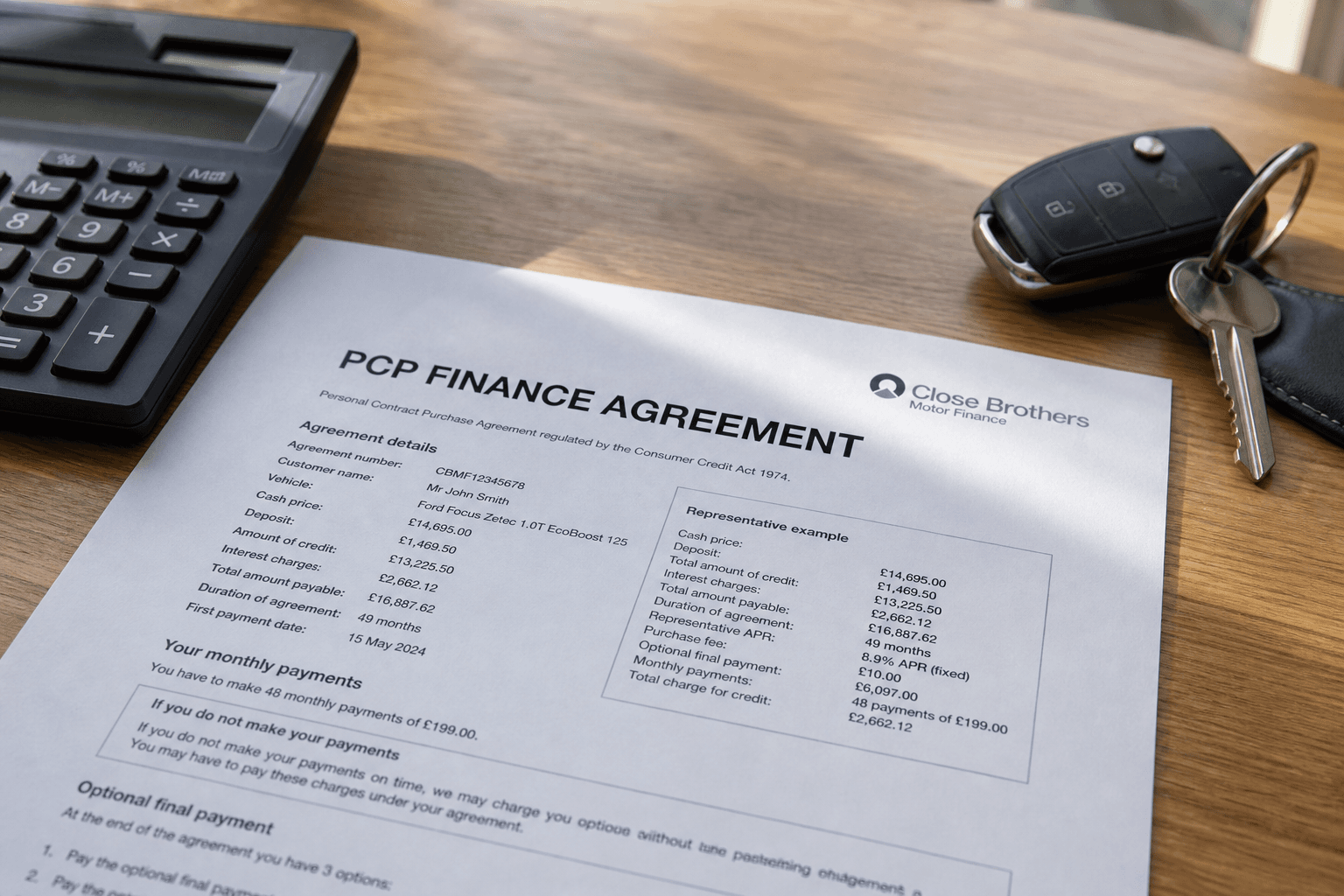

Personal Contract Purchase (PCP) spreads the cost of a car across monthly payments, but the buyer does not own the car during the agreement. The finance company retains ownership.

At the start, the car is valued at its current price. A projected future value (called the Guaranteed Minimum Future Value, or GMFV) is calculated for the end of the term. The buyer pays the difference between those two figures, plus interest, spread across the monthly payments.

At the end of the term, the buyer owes one large final payment - the balloon - to own the car outright. Most buyers do not pay it. They either hand the car back or use any equity to fund the next deal.

Why PCP Creates Risk When Buying Used

Here is the problem: if a buyer on a PCP deal sells the car privately before the agreement ends, they are selling a car they do not own. The finance company still has a legal charge against the vehicle.

You buy the car in good faith. The previous keeper pockets your money. The finance company does not get paid. The finance company can legally repossess the car from you.

This is not theoretical. It happens regularly. The buyer who paid for the car loses the car and has no easy route to recover the money.

How Common is This?

Around one in six used cars in the UK has outstanding finance registered against it. PCP is the most common source. This statistic is the reason finance checks exist.

What Hire Purchase (HP) Means Compared to PCP

HP is simpler. You pay monthly instalments and own the car outright at the end. There is no balloon payment and no option to hand back. The finance company still owns the car during the agreement, so the same risk applies if the car is sold privately before the deal ends.

How to Protect Yourself

Check the finance status before you hand over any money. A history check at check.bad-drivers.uk searches the HPI finance register and shows whether any finance is registered against the vehicle.

If the check shows outstanding finance, you have two options. Walk away. Or contact the finance company, confirm the settlement figure, and arrange for the finance to be settled directly from the sale proceeds before any money reaches the seller.

Never buy a car with outstanding finance on the seller's promise that they will pay it off. Get it settled in writing before the transaction completes.

Useful Links

- FCA guidance on car finance - How PCP and HP are regulated in the UK

- Citizens Advice - problems with car finance - What to do if a financed car is repossessed

- The Money Advice Service - Independent explanation of PCP agreements