A logbook loan could cost you the car you just paid for. This is not a theoretical risk - it happens every year to buyers who did not check before they bought.

What Is a Logbook Loan?

A logbook loan is a type of secured borrowing where the lender takes a legal interest in a vehicle using a document called a bill of sale. The borrower hands over the V5C logbook as part of the process - which is where the name comes from.

Unlike most forms of finance, the borrower keeps the car and continues to drive it. The lender holds the bill of sale, which gives them a legal claim to the vehicle if the loan is not repaid.

Logbook loans are regulated by the Financial Conduct Authority (FCA) but the protections for private buyers are weaker than with hire purchase (HP) finance.

Why Logbook Loans Are Dangerous When Buying Used

With hire purchase finance, private buyers are generally protected by Section 27 of the Hire Purchase Act 1964. If you buy a car from a private seller without knowing about HP finance, you often get to keep the car.

Logbook loans work differently. The bill of sale is a separate legal instrument registered under the Bills of Sale Acts. In many cases, the lender's interest in the vehicle survives the sale. That means even if you bought the car in good faith and paid full market value, the lender may still be able to repossess it.

The Financial Conduct Authority has recognised this as a problem and rules have been tightened, but logbook loans taken out before recent regulatory changes may still carry this risk.

How Logbook Loans Get Hidden

A seller who has a logbook loan outstanding may:

- Present the V5C as if the car is fully theirs to sell

- Claim they lost the V5C and offer to apply for a replacement

- Price the car attractively to move it quickly

None of these are automatic signs of fraud. But if a seller is evasive about finance, pushes for a quick sale, or cannot produce the V5C, you need to investigate before you commit.

What a Bill of Sale Looks Like in Practice

When a logbook lender registers a bill of sale, it is recorded at the High Court. This was traditionally done using physical paper records, which made searching them difficult for ordinary buyers.

Modern vehicle history checks search finance databases that include bills of sale. This is the practical way to find out whether a logbook loan exists against a vehicle before you buy.

Checking for a Logbook Loan Before You Buy

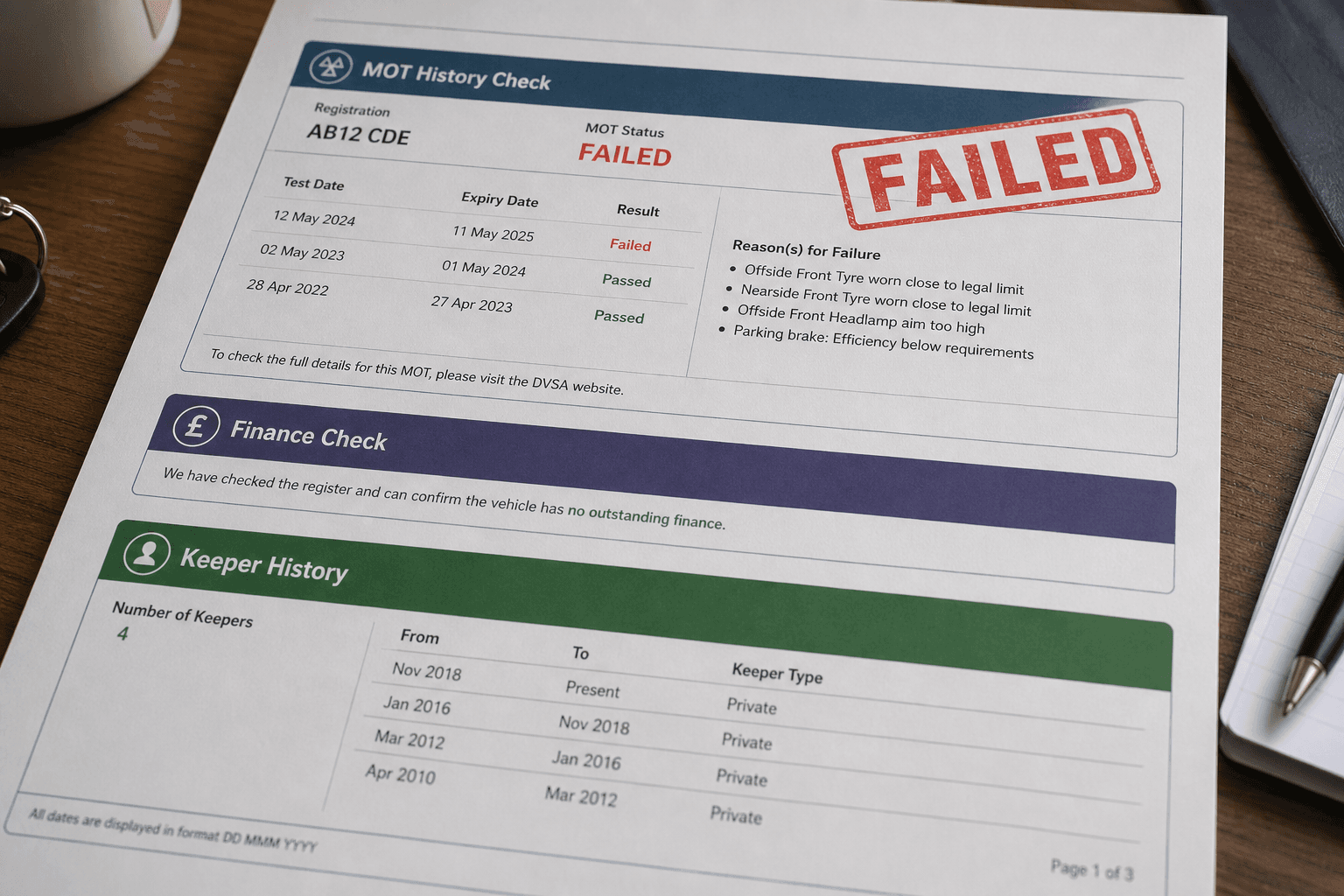

Run a vehicle history check before you hand over any money. A full check at check.bad-drivers.uk searches multiple finance databases and flags any outstanding logbook loan or bill of sale against the vehicle.

This check covers:

- Outstanding hire purchase and PCP finance

- Logbook loan bills of sale

- Stolen markers

- Write-off and insurance total loss records

- Keeper history and plate changes

The check takes seconds. Losing a car to a lender you did not know existed can cost thousands.

What to Do If You Find a Logbook Loan

If a history check shows an outstanding logbook loan, do not complete the purchase until the loan is cleared.

Ask the seller to provide written confirmation from the lender that the debt has been settled and the bill of sale discharged. Get this before you hand over money, not after.

If the seller claims there is no loan but the check shows otherwise, walk away. Trusting a seller's word over a database record is how people lose cars.

Logbook Loans vs Other Finance Types

| Finance type | Buyer protection if bought privately | |---|---| | Hire Purchase (HP) | Generally protected under HPA 1964 s.27 | | PCP | Generally protected under HPA 1964 s.27 | | Logbook loan (bill of sale) | Weaker - lender's claim may survive sale | | Personal loan (unsecured) | Car is not security - no lender claim |

A personal loan secured against nothing is not a problem for a car buyer. A logbook loan is. That distinction matters when you are searching for finance on a used car.

FAQ

What is a logbook loan on a car?

A logbook loan is a type of secured loan where the lender holds a bill of sale against the vehicle. The borrower keeps the car but the lender has a legal claim on it until the loan is repaid. If the loan is not repaid, the lender can repossess the car.

Can a lender take a car I bought in good faith?

Yes, in many cases they can. Logbook loans use a bill of sale, which is a form of security that does not always give a private buyer the same protection as HP finance. The lender's claim on the vehicle may survive the sale.

How do I check if a car has a logbook loan against it?

Run a full vehicle history check. A check at check.bad-drivers.uk searches finance databases including bills of sale to flag any outstanding logbook loan before you hand over money.

Useful Links

- Logbook loans explained - FCA - Regulator guidance on logbook loan protections

- Bills of Sale - Citizens Advice - What a bill of sale means and how it works

- Buying a used car - Citizens Advice - Your rights when buying used