Buyers find out the car they just purchased costs twice what they budgeted to insure. It happens constantly, and the car insurance group is almost always the reason nobody checked.

What Is a Car Insurance Group?

Every car sold in the UK is assigned an insurance group from 1 to 50 by Thatcham Research, an independent motor insurance research centre. The system is used by virtually every UK insurer to set premiums.

Group 1 represents the cheapest cars to insure. Group 50 represents the most expensive. The difference in annual premium between a group 1 and a group 50 car can be thousands of pounds, even for the same driver with the same record.

The car insurance group is set at model and trim level, not just make and model. Two versions of the same car - one with a 1.0-litre engine and one with a 2.0-litre turbocharged engine - will sit in different groups. Spec matters.

How Is the Insurance Group Calculated?

Thatcham assigns each car a group based on several factors:

Repair costs. Cars with expensive parts or complex bodywork cost more to repair after a collision. Higher repair costs mean a higher insurance group.

New car value. More expensive cars attract higher settlement costs after a total loss. This pushes the group up.

Performance. Higher top speeds and faster acceleration increase the statistical risk of accidents and raise the group.

Security. Cars with Thatcham-approved alarms, immobilisers, and tracking devices may receive a lower group rating. Cars with weak factory security receive a higher one.

Parts availability. If replacement parts are rare, expensive to import, or only available from main dealers, repair costs rise and the group follows.

Bumper compatibility. Thatcham tests how well a car's bumpers survive low-speed impacts. Poor results push the group up.

Each group number may also carry a letter: E (exceeded), A (acceptable), or U (unacceptable for security). An E suffix means the car exceeded the security requirement for its group. A U suffix means it fell short.

Why This Matters When Buying Used

The insurance group does not change with age. A car that was group 35 when new is still group 35 ten years later, regardless of its depreciated value.

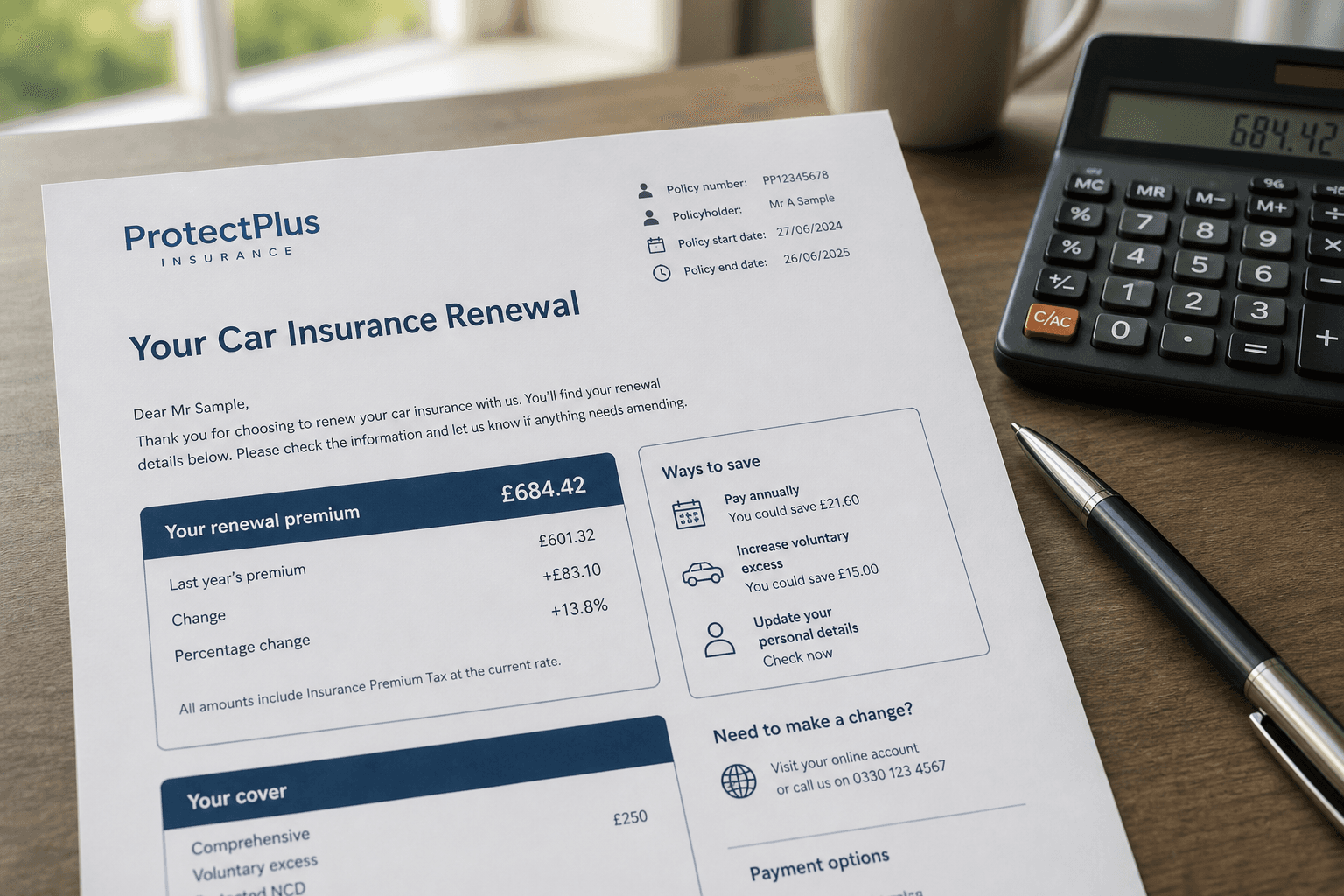

This catches buyers who focus on the purchase price and forget the running costs. A car at £6,000 that sits in group 40 will cost significantly more to insure than a similarly priced car in group 20. Over three years of ownership, the insurance difference can easily exceed the price gap between two comparable cars.

Before you make an offer, check the group. If it is higher than you expected, get an actual insurance quote for that specific registration. Comparison sites will show you the real cost in minutes.

Trim Level and Engine Size Change Everything

The same model can span ten or more groups depending on specification. A base-trim supermini with a 1.0-litre engine might sit in group 5. The same model in a hot hatch trim with a 1.6-litre turbocharged engine might sit in group 30.

When you check a car's insurance group, you need the exact trim level and engine variant - not just the model name. A full vehicle history check at check.bad-drivers.uk returns the complete factory specification including engine size, trim, and options, giving you what you need to get an accurate group rating and insurance quote.

What a High Insurance Group Can Mean for Young Drivers

For drivers under 25, insurance group has an outsized effect on premiums. An older driver in a group 20 car may pay £600 a year. A 19-year-old in the same car might pay £2,000 or more.

Move that young driver into a group 35 car and the premium can become unaffordable, or the insurer may decline the risk entirely.

If you are buying for a young driver, or if you are a young driver buying for yourself, use group 1 to 10 as a starting target. The choice of car will have more impact on your insurance bill than almost anything else you do.

Modifications and Insurance Groups

Non-standard modifications alter how insurers view a vehicle. Lowered suspension, non-standard alloys, engine remaps, and body kits all affect the risk profile.

In some cases, modifications push the car into a higher group. In others, an insurer will refuse to cover the car at all, or will only cover it under a specialist policy at a significantly higher premium.

If the car you are looking at has been modified, check how those modifications affect the insurance group before you commit. And make sure any modifications are declared - failing to disclose them can invalidate a claim.

How to Check a Car's Insurance Group Before Buying

- Get the exact make, model, engine size, and trim level from the seller or from the V5C.

- Go to the Thatcham Research website or a comparison site group checker and enter the details.

- Get an actual insurance quote using your own details before you commit.

Do not assume. Check.

FAQ

What is a car insurance group in the UK?

Every car sold in the UK is assigned an insurance group from 1 to 50 by Thatcham Research. Group 1 is the cheapest to insure. Group 50 is the most expensive. The group is based on the car's repair costs, performance, safety features, and parts availability.

How do I find out what insurance group a car is in?

You can check a car's insurance group free at the Thatcham Research website or through comparison sites. Enter the make, model, and trim level. A full vehicle history check at check.bad-drivers.uk shows the full spec including engine size and trim, which determines the group.

Does the insurance group change if the car has been modified?

Yes. Non-standard modifications can push a car into a higher insurance group or cause some insurers to refuse cover entirely. Always declare modifications and check how they affect the group rating before buying a modified car.

Useful Links

- Insurance group checker - Thatcham Research - Official group ratings for every UK car

- Car insurance explained - Citizens Advice - Your rights and what insurers must tell you

- Motor insurance regulation - FCA - FCA rules on how motor insurance is priced and sold