Selling a car with outstanding finance is not straightforward. In most cases, doing it without settling the finance first is illegal - and it puts the buyer at serious risk of losing the car with no recourse against you.

This is a common situation. Millions of UK drivers have cars on hire purchase or PCP agreements. If you need to sell before the agreement ends, there are legal routes. Quietly selling the car and keeping the proceeds is not one of them.

Who Actually Owns the Car?

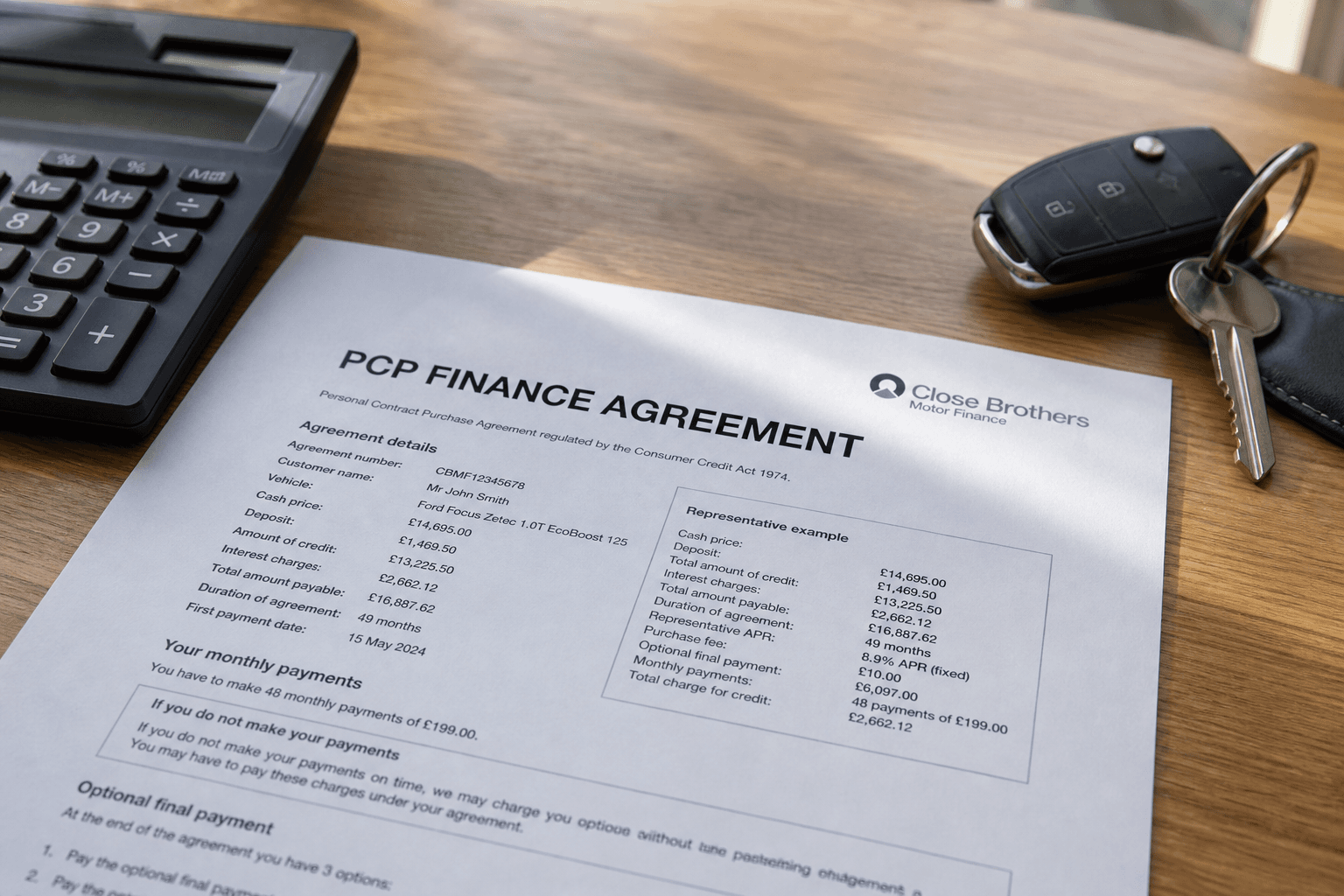

On a hire purchase (HP) or conditional sale agreement, the finance company owns the car. You have possession and the right to use it, but legal title does not pass to you until the final payment is made.

On a personal contract purchase (PCP) agreement, the same applies. Until you make the optional final payment (the balloon), the finance company still owns the car.

On a personal loan, the situation is different. You borrowed money, bought the car outright, and you own it. The lender has a claim on you personally, not on the vehicle. You can sell the car, although the debt remains.

What Happens If You Sell Without Settling?

If you sell a car on HP or conditional sale without settling the finance, the finance company can repossess the car from the new owner. They do not need to pursue you first.

The buyer loses the car. If they paid you £10,000, they have a claim against you personally - but recovering money through the courts takes time and is not guaranteed, particularly if you no longer have the funds.

This is fraud under the Fraud Act 2006. Knowingly misrepresenting your right to sell is a criminal offence, not just a civil matter.

The Right Way to Sell a Car With Finance

Option 1: Settle the finance before selling.

Contact your finance company and ask for the settlement figure. This is the amount that will fully close the agreement. Once you pay it, you own the car outright and can sell it to anyone.

If the car is worth more than the settlement figure, the difference is yours. If the settlement figure is more than the car is worth, you are in negative equity - you will need to pay the shortfall from other funds before you can sell.

Option 2: Use a dealer part-exchange.

A legitimate dealer will often settle outstanding finance as part of a part-exchange. They contact the finance company, pay the settlement, and deduct it from the part-exchange value. This is standard practice and fully legal.

Option 3: Voluntary termination.

Under the Consumer Credit Act 1974, if you have paid at least 50% of the total amount payable - including all interest and charges - you have the right to return the car to the finance company and terminate the agreement. You walk away owing nothing more.

If you have not reached 50%, you can still apply to terminate, but you will need to top up to the 50% threshold first.

Voluntary termination does not put cash in your pocket. You simply hand the car back. But if the car is worth less than the remaining finance and you cannot cover the shortfall, it may be the cleanest option.

Option 4: Sell subject to finance settlement with buyer's agreement.

Some private sales are structured so the buyer pays the settlement figure directly to the finance company and the balance to the seller. This requires the buyer's full understanding and agreement, and you should get everything in writing.

This only works if the buyer is willing to take the risk of coordinating payment. Most are not.

Negative Equity

Negative equity means you owe more on the finance than the car is worth. It is common on PCP agreements where large balloon payments are involved.

In negative equity, your options are:

- Pay the shortfall and settle, then sell

- Continue making payments until equity improves

- Voluntary termination if you meet the 50% threshold

- Speak to the finance company about refinancing

There is no legal way to sell the car and leave the debt with someone else on an HP or conditional sale agreement.

How Buyers Can Protect Themselves

If you are buying privately, run a vehicle history check before paying anything. A full check will show whether the car has outstanding finance registered against it.

Knowing about the finance before you buy gives you options. You can negotiate a structured settlement, walk away, or ask the seller to provide proof of clearance before you hand over money.

Finding out after the fact - when the finance company is at your door to repossess - leaves you with a legal dispute and no car.

Useful Links

- Consumer Credit Act 1974 - voluntary termination rights - The statutory right to terminate a regulated credit agreement

- Hire Purchase Act 1964 - Protections for private buyers who purchase a car in good faith

Run a full vehicle history check for £9.99. Finance check, write-off category, stolen marker, keeper history and more. Find out before you buy.

FAQ

Can you legally sell a car with outstanding finance?

Not without the finance company's consent. On hire purchase and conditional sale agreements, the lender owns the car until the final payment. Selling it without settling the finance or getting explicit lender permission is fraud, and the finance company can repossess the car from the buyer.

What is the settlement figure on a car finance agreement?

The settlement figure is the exact amount needed to fully pay off and close the finance agreement early. It may include an early repayment charge. You can request it directly from your finance company at any time. It is valid for a set number of days, typically 10 to 28.

What is voluntary termination?

Voluntary termination is a legal right under the Consumer Credit Act 1974. If you have paid at least 50% of the total amount payable (including interest and charges), you can return the car to the finance company and walk away with nothing further owed. It is not the same as selling the car.

How can buyers check for outstanding finance?

Run a vehicle history check before buying. A full check includes a finance search that shows whether the car has outstanding hire purchase, PCP, or other finance agreements registered against it.