Hire purchase, usually called HP, is one of the most common ways to finance a car in the UK. You make fixed monthly payments, and at the end of the agreement, you own the car outright. Simple in theory, but there is a catch that catches out a lot of used car buyers: until that final payment is made, the finance company owns the car, not the person driving it. Run a free check at check.bad-drivers.uk before you buy, to see if any finance is still outstanding on the car.

How Hire Purchase Actually Works

HP is a secured loan. The lender buys the car and hires it to you. You make fixed monthly payments over an agreed term, typically two to five years. At the end, you make a final payment (usually just an option-to-purchase fee, often around £100 to £200) and ownership transfers to you.

There is no large balloon payment at the end, which is the main difference from PCP. The monthly payments on HP are usually higher than PCP for the same car and term because you are paying off the full value of the vehicle, not just its depreciation.

You also have no mileage limits with HP. PCP agreements restrict your annual mileage and charge per mile over the limit. HP has none of that.

Who Provides HP Finance?

HP is offered by banks, specialist motor finance companies, and through dealerships acting as credit brokers. When you buy from a dealer, the HP agreement is often arranged on the spot as part of the purchase. The car is registered in your name but the finance company holds legal title until the debt is cleared.

Hire Purchase vs PCP: What Is the Difference?

Both HP and PCP let you drive a car while paying monthly. The differences matter when it comes to ownership, payments, and flexibility.

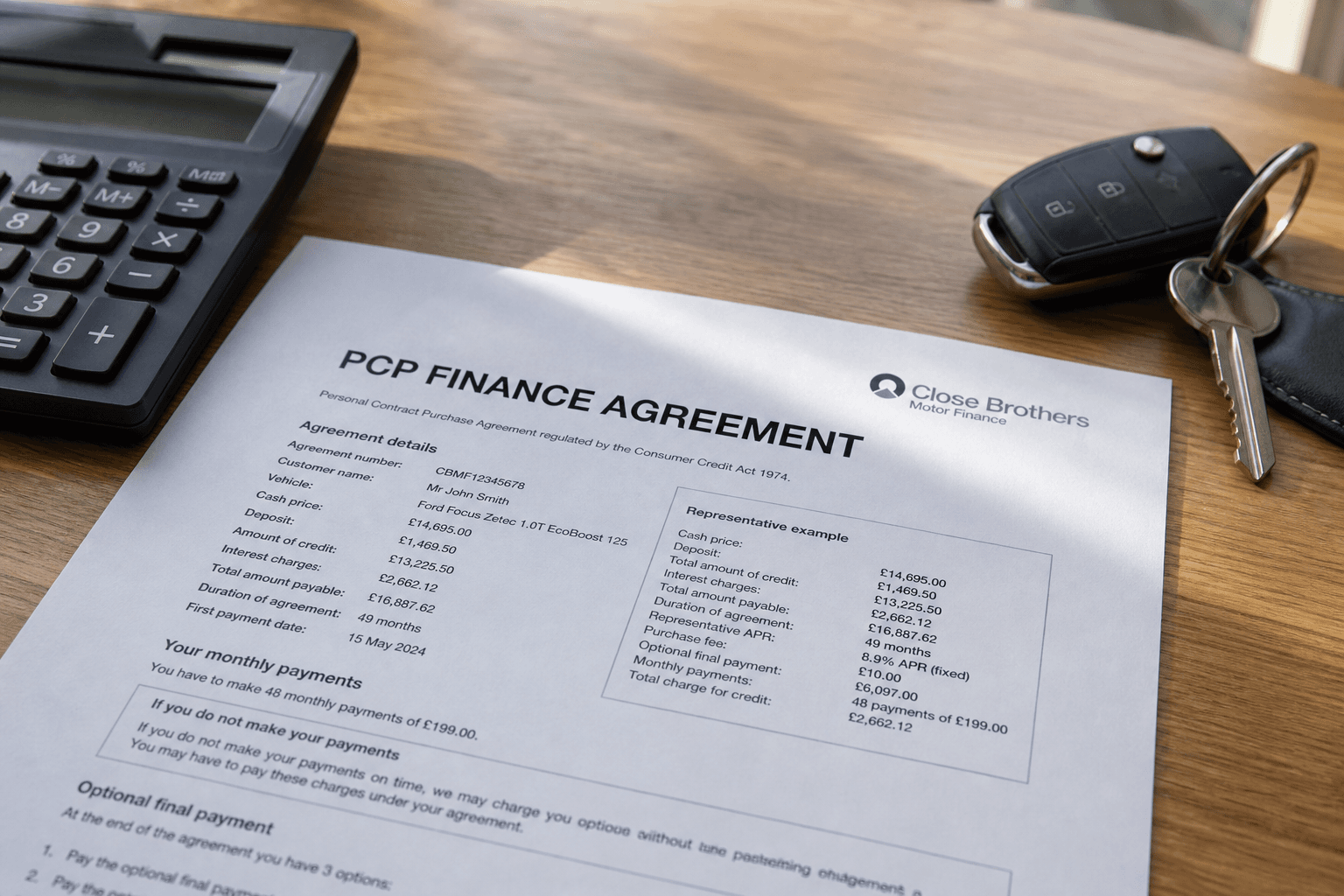

With PCP, part of the car's value is deferred to the end of the agreement as a guaranteed minimum future value, called the balloon payment. Your monthly payments are lower because you are only financing the depreciation. At the end, you can pay the balloon and keep the car, hand the car back, or use any equity as a deposit on a new deal.

With HP, you finance the entire value of the car from the start. Monthly payments are higher, but there is no balloon payment decision at the end. You just own it.

PCP gives you more flexibility but leaves you with a large payment decision at the end. HP is more straightforward. You pay, you own it, done.

What Happens If You Buy a Car With HP Outstanding?

This is where it gets serious for used car buyers. If someone sells you a car that still has HP finance outstanding, you are buying a car the seller does not legally own. The finance company still owns it.

Under the Bill of Sale Act and the Consumer Credit Act, the finance company can repossess the vehicle from you even if you paid the seller in good faith. You lose the car and your money. Your claim is against the seller, who may well be untraceable or unable to pay.

There is one legal protection available to private buyers: the principle of good faith purchase under the Hire Purchase Act 1964. If you are a private individual (not a motor trader) and you buy the car in good faith without knowing about the HP, you may be able to keep the car if the finance company pursues the matter. But this is not guaranteed, it applies only to private buyers, and it still involves legal proceedings.

The safest thing is to check before you buy.

How to Check If a Car Has HP Finance on It

A full vehicle history check will show whether any outstanding finance is registered against the car. Finance agreements are recorded on databases including HPI and Experian, and a check will flag any live agreements.

Run a check at check.bad-drivers.uk before you agree to buy. The check takes seconds and covers outstanding finance, stolen markers, write-off history, and keeper records.

If the check shows finance outstanding, do not hand over money until the seller can demonstrate it has been cleared. The safest route is to contact the finance company directly to confirm the settlement amount, and to pay the settlement to them, not to the seller. Get confirmation of settlement in writing before the funds leave your account.

Some sellers genuinely do not know their car has finance outstanding, especially if it was a previous keeper's agreement that was not fully settled. The history check will tell you regardless of what the seller says.

Is HP a Good Way to Finance a Used Car?

HP is straightforward and predictable. Fixed payments, no mileage restrictions, no balloon payment gamble at the end. If you want to own the car at the end of the agreement without any ambiguity, HP does that cleanly.

The downsides are the higher monthly payments compared to PCP on the same car, and the fact that you are tied in for the full term without the flexibility to hand the car back easily in the way PCP allows.

Under Section 99 of the Consumer Credit Act, you do have the right to voluntarily terminate an HP agreement once you have paid at least 50 percent of the total amount payable. You hand the car back and owe nothing more. Below 50 percent, you would need to make up the shortfall to terminate. This is a legal right and cannot be removed by the finance company.

If you are considering HP on a used car through a dealer, make sure you are shown the full cost of credit, the total amount payable, and the APR. Compare those figures before signing anything.

What to Do If You Have HP and Want to Sell

You cannot sell a car with outstanding HP without the finance company's permission. The car is not yours to sell.

The way to handle it is to request a settlement figure from the finance company. That is the amount required to pay off the agreement early. Once that is paid, you will receive a letter confirming the finance is cleared and the title transfers to you. You can then sell freely.

If you sell privately and the buyer runs a history check, the outstanding finance will show up. Most buyers will refuse to proceed until it is cleared, or will insist on paying the settlement directly to the finance company as part of the transaction.

Useful Links

- Gov.uk: Hire purchase and conditional sale — your rights under the Consumer Credit Act for HP agreements

- Gov.uk: Voluntary termination of car finance — the right to hand back a car once 50 percent of the total is paid

- Gov.uk: Consumer rights when buying goods — protections when purchasing from a dealer

Run a full vehicle history check at check.bad-drivers.uk for £9.99. Outstanding finance, stolen marker, write-off history, keeper records, and MOT history. Know before you buy.

Frequently Asked Questions

What is hire purchase on a car?

Hire purchase is a finance agreement where the lender buys the car and you hire it over a fixed term with monthly payments. At the end of the agreement, you pay a small option-to-purchase fee and ownership transfers to you. You do not own the car during the HP term, the finance company does.

What is the difference between HP and PCP?

HP spreads the full cost of the car over fixed monthly payments with no balloon at the end. PCP defers a chunk of the car's value to a balloon payment at the end, giving lower monthly payments but leaving you with a decision to make when the term ends. HP is simpler and gives you ownership at the end without any ambiguity.

Can I buy a car that still has HP on it?

You can, but you must clear the finance as part of the transaction. Never pay the seller and trust them to clear the HP themselves. Contact the finance company to confirm the settlement figure and pay it directly to them. Get written confirmation that the finance is cleared before the car changes hands. If you buy without checking and the HP is still live, the finance company can repossess the car from you.

How do I check if a car has HP finance?

Run a full vehicle history check before you buy. Finance agreements including HP are recorded on insurance and finance databases and will show on a history report. The check will tell you if there is live finance registered against the car and with which company.

Can I sell my car if it has HP outstanding?

Not without clearing the finance first. The car belongs to the finance company until the agreement is settled. Request a settlement figure, pay it to the lender, and get written confirmation before you attempt to sell. Selling a car you do not own is a criminal offence.

What is voluntary termination on HP?

Under Section 99 of the Consumer Credit Act, you have the legal right to return a car on HP once you have paid at least 50 percent of the total amount payable under the agreement. You hand the car back in reasonable condition and owe nothing more. Below 50 percent, you would need to top up the payments to reach that threshold first.