GAP stands for Guaranteed Asset Protection. It is an add-on insurance product that covers a specific financial gap that standard car insurance does not address.

Understanding what GAP insurance covers and when to buy it saves you money on unnecessary products and protects you when the risk is real.

The Problem GAP Insurance Solves

Standard comprehensive car insurance pays out the current market value of your car if it is written off or stolen. That sounds fair until you see what it means in practice.

You buy a new car for £25,000. You put down £3,000 and finance the rest on PCP. Two years later, the car is written off. Your insurer pays out £17,000 - the current market value. But you still owe £20,000 on the finance agreement.

You are left £3,000 short. You have no car and still owe money you no longer have an asset to show for.

GAP insurance covers that shortfall.

Types of GAP Insurance

Return to Invoice GAP. Pays the difference between your insurer's payout and the original invoice price of the car. If you paid £25,000 and your insurer pays £17,000, RTI GAP pays £8,000.

Finance GAP. Pays the difference between your insurer's payout and the amount still outstanding on your finance agreement. Protects you from negative equity after a write-off or theft.

Vehicle Replacement GAP. Covers the difference between your insurer's payout and the cost of a new equivalent replacement vehicle.

Who Needs It?

GAP insurance is relevant for:

New car buyers on PCP. PCP finance is structured so that you owe most of the car's value in the early years while the car depreciates quickly. The gap between what you owe and what the car is worth can be significant in years one to three.

Anyone who put minimal deposit down. Low or zero deposit means high outstanding finance from day one.

Buyers of cars that depreciate sharply. Some models lose 30 to 40 percent of their value in the first two years.

Who Probably Does Not Need It

Used car buyers paying cash. If there is no finance and you are not dependent on getting the full purchase price back, there is no gap to cover.

Buyers with significant equity. If you put down a substantial deposit and the outstanding finance is comfortably below the car's market value, GAP insurance is covering a risk that does not really exist.

Those buying older, lower-value cars. The premium cost of GAP insurance relative to the potential shortfall is less favourable on lower-value vehicles.

Cost and Where to Buy

Dealers will offer GAP insurance at the point of sale, typically priced at £300 to £500 added to the finance. You can buy it independently for less. Several specialist providers offer equivalent products at lower prices. Do not accept the dealer's quote without shopping around.

GAP insurance is typically only available within a set period of purchasing the vehicle - often 180 days or less. Act quickly if you decide you need it.

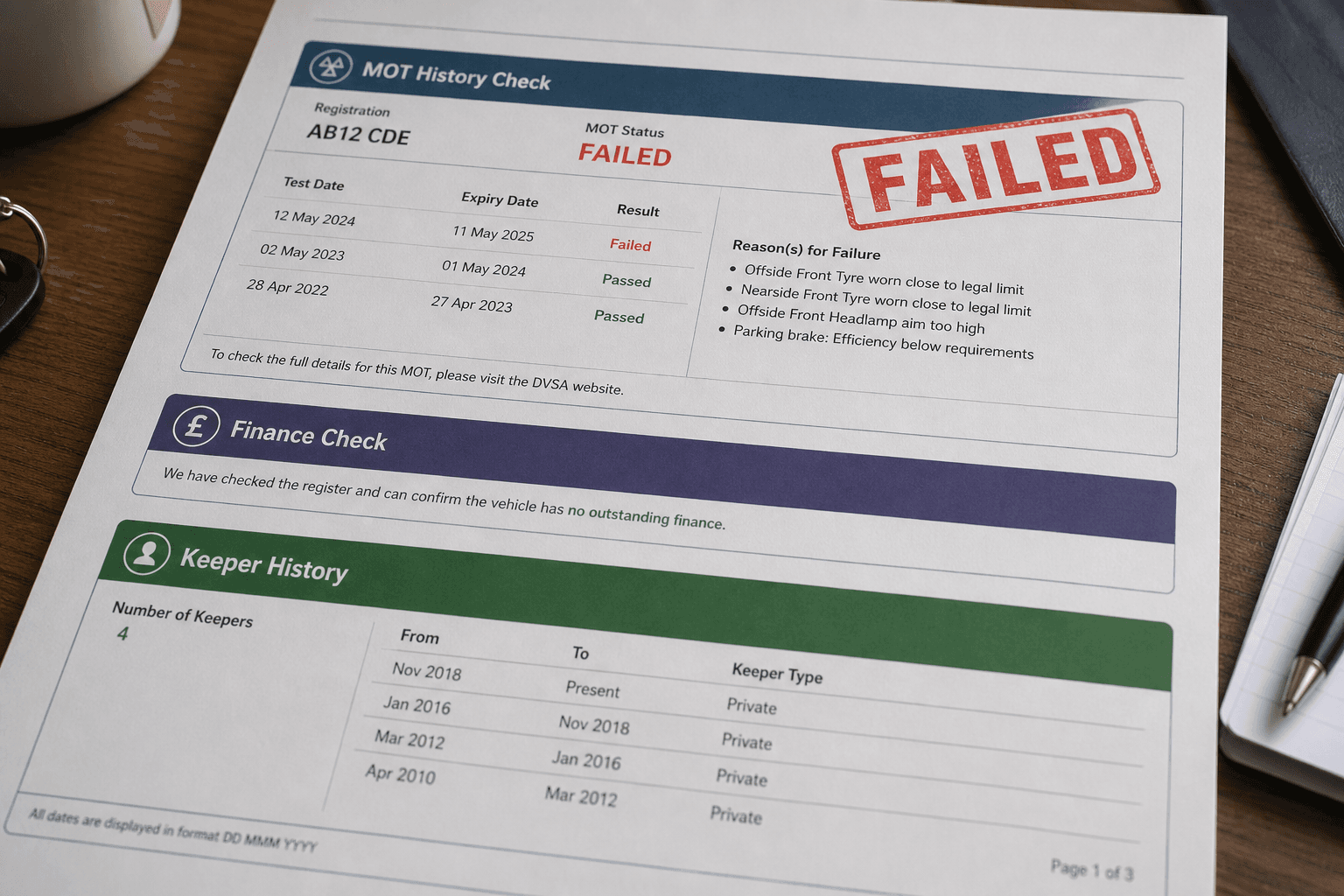

Before buying any car, run a history check at Bad Drivers UK to confirm the vehicle is clean before you invest in additional protection products.

FAQ

What does GAP insurance actually cover?

GAP insurance covers the difference between what your insurer pays out after a write-off or theft (current market value) and either your outstanding finance balance (finance GAP), your original invoice price (return to invoice GAP), or the cost of a replacement vehicle (vehicle replacement GAP).

Is GAP insurance worth buying from the dealer?

Dealer-sold GAP insurance is typically priced at £300 to £500 added to the finance, which is expensive. You can buy equivalent cover independently for significantly less. Always compare quotes before accepting the dealer's offer.

Do you need GAP insurance if you are buying with cash?

No. GAP insurance protects against a shortfall between the payout and what you owe. If there is no finance there is no shortfall - your insurer pays current market value, which is close to what you paid for a recent purchase. Cash buyers can skip it.